With more than 38 million unemployed and the economy shrinking by 4.8% (per the US BEA data), the impact of the COVID-19 pandemic on the US has been unprecedented.

Even as the death toll crossed a psychological landmark of 100,000 many businesses across the US are planning a phased reopening, albeit with adequate precautions.

However, this may hardly bring cheer to the banking and financial services industry that is facing a bleak H2 this year.

The high unemployment caused by the pandemic has imposed hardships on Americans and many will find it difficult to meet their financial obligations, despite the forbearance that lenders have provided them. The result will be a sharp rise in delinquencies and charge offs across lending products.

Further, the high expected losses will also force banks to apportion higher capital reserves against losses.

According to a recent McKinsey study, the expected losses to US retail lending business in the US in the short term (three to six months) could be between $15 -$25 billion. If unemployment hits 20%, the longer term losses could be over $150 billion over the next two years.

It is difficult to imagine such a huge loss staring at the retail banking industry. Whether this actually pans out or not will largely depend on how robustness of the recovery of the US economy and to some degree on how smartly lending institutions manage their credit risk policy during these turbulent times.

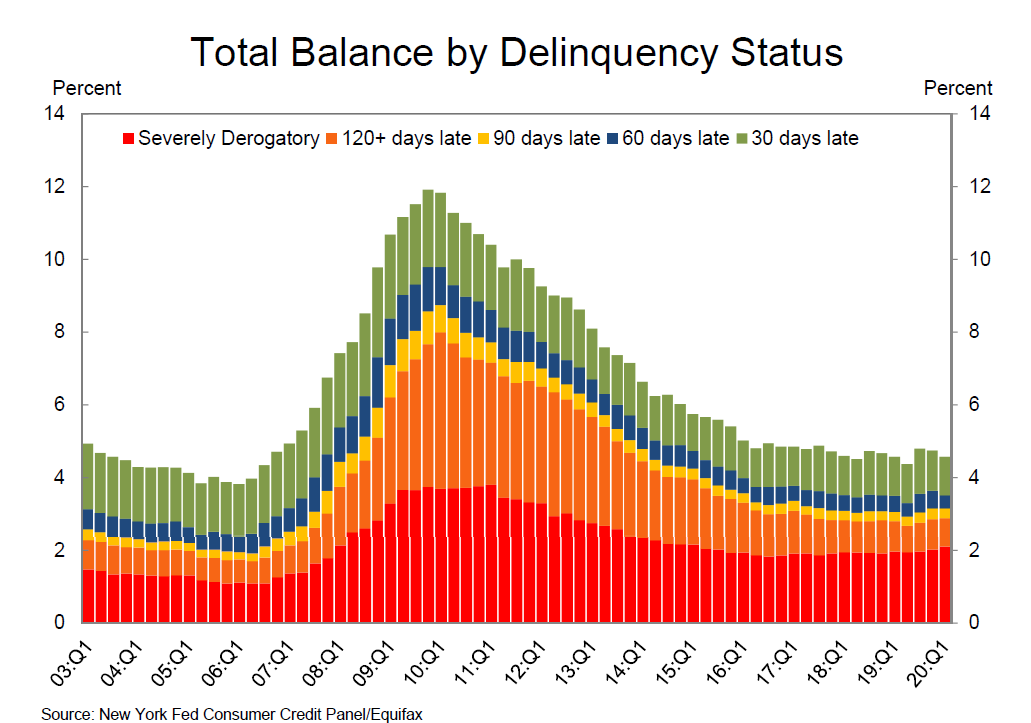

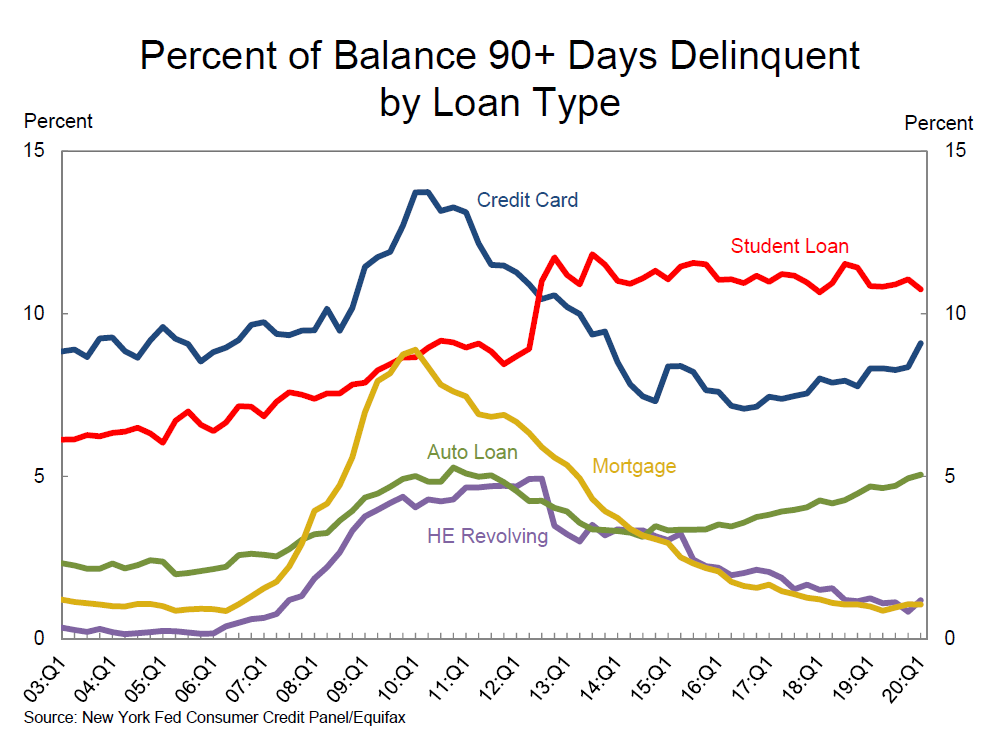

But all is not lost. There may be a silver lining that cannot be ignored. Available data points to an otherwise healthy economy prior to the pandemic. Data published by the Federal Reserve Bank of New York (May 20202) shows that non housing debt at the end of Q1 2020 was flat, punctuated by a seasonal decline in credit card debt of $34 billion. This drop was significantly larger than the decline for the same period in 2019.

Obviously the data published by the Federal Reserve does not incorporate the impact of COVID-19 on the economy. But the point to note here is that as at the end of Q1 2020, there were no major concerns with respect to consumer debt.

The insight here is that if the US can manage an orderly reopening of the economy and reign in unemployment, even if slowly, there is every chance that the economy will recover faster than many are forecasting. That would be good news for the banking and financial services industry.