PM Images

Investment thesis

I continue to think that the Nu Holdings (NYSE:NU) investment case remains compelling as valuations have come down while the fundamentals of the company continue to improve. The article will illustrate just how the business fundamentals of the company has improved, and my investment case for Nu is as follows:

Nu continues to be a well-positioned fintech in Latin America that is able to bring value add to different customer segments in the region by removing pain points and bringing innovation to the financial services market. The company has best-in-class net promoter scores across markets, which highlights strong customer satisfaction and loyalty and the existing customer base acts as a marketing tool to bring in new customers through word of mouth. While Nu boasts strong revenue growth, the company has a visible and solid model for improving operating leverage and profitability of the company while continuing to invest in the long-term value creation of the company.

I have written an initiation article to introduce Nu and a subsequent article detailing its strong execution in volatile markets.

A business model made to weather cycles

I think that one of Nu has demonstrated well in its operating history that it has the track record to operate and grow through market cycles. The company went through the largest recession in Brazil’s history when GDP contracted by 7% from 2015 to 2016, as well as multiple political changes in the 3 countries in which it operates in. While 2021 may be a slightly more volatile market environment, I am of the view that Nu will be able to tide through this and leverage on the opportunities of today to bring in long-term value.

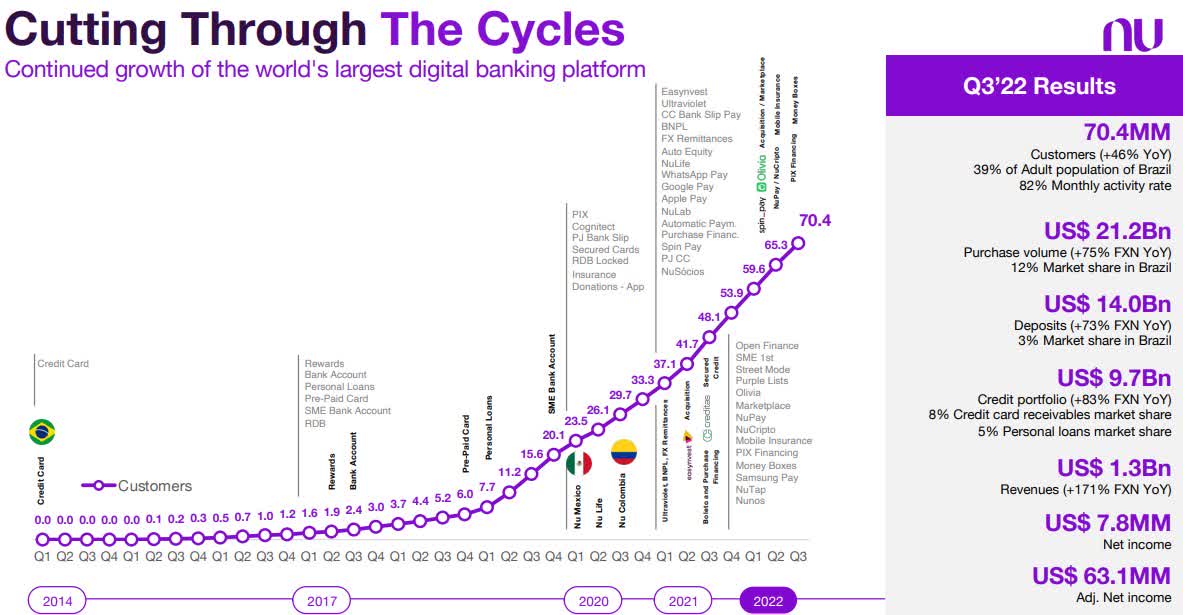

Nu’s resilient performance across cycles (Nu IR)

As can be seen highlighted in the figure above, Nu grew revenues by 171% year on year, which is very impressive in the current macro environment as management continues to demonstrate good execution in uncertain times. Furthermore, the company posted a net income of $7.8 million and an adjusted net income of $63.1 million for the third quarter of 2022.

In terms of operational metrics, the company added more than 5 million new customers in the quarter and has slightly more than 70 million customers today, up 46% year on year. This represents 39% of the adult population in Brazil and its customers have an 82% monthly activity rate, which is a new high. With its 70 million customers across the 3 countries it operates in, the company is now the 6th largest financial institution in Latin America by active customers. Nu’s purchase volume was up 75% year on year to $21 billion, representing a market share of 12% in Brazil. In addition, despite increasing the resilience of its credit underwriting to account for the more volatile market environment, Nu’s credit portfolio continues to grow at 83% year on year to about $10 billion. This growth is fully funded by Nu’s own retail deposits that grew to $14 billion in the third quarter of 2022. The company demonstrated its ability to balance growth and profitability while continuing to improve on engagement and operational metrics.

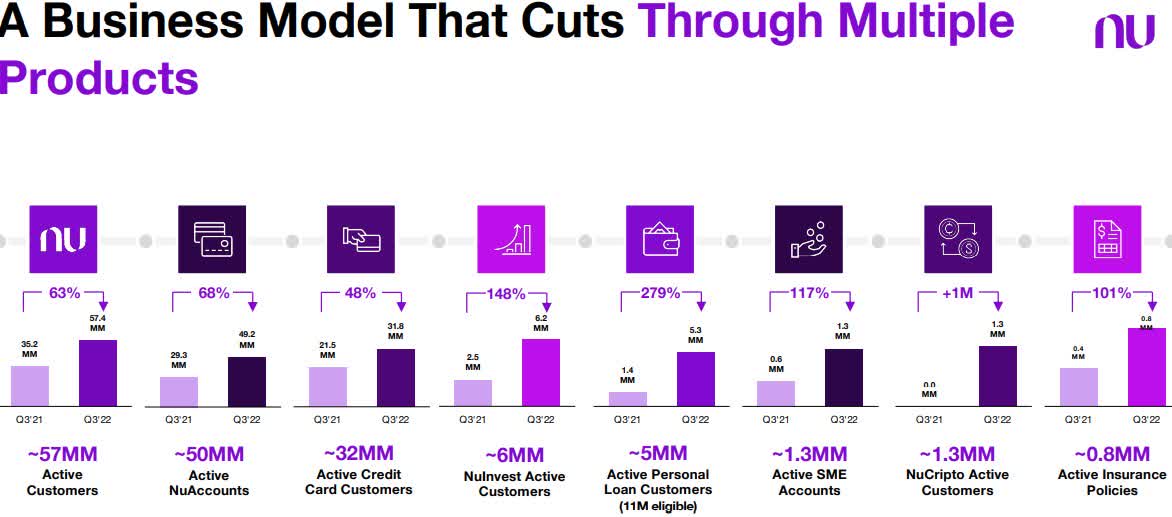

Nu’s management team is looking to build the business into a platform that spans multiple products, multiple countries, and multiple segments. At the end of the day, this results in a financial services platform that is well diversified across products, countries and segments that is able to weather volatile market conditions. As can be seen below, Nu has 8 main products that are in various stages of growth and maturity. The idea here is for Nu to not just maintain but continue to develop and grow new innovative products that add value to its customers and contribute a net positive effect to the company’s Net Promoter Score. I think that we have seen Nu accelerate the pace at which it has developed and launched new products into the market due to the increased focus on investments into the company and the platform. New products launched will bring new growth engine for the business and drive it towards long-term value addition.

Business model: Multiple products (Nu IR)

The next focus for management is to expand into multiple countries and become a multi-country platform. Mexico and Colombia are relatively new markets for Nu as the company entered the markets in 2019 and 2020 respectively. As a result, they represent the next growth driver for Nu as they continue to have strong growth potential given the early success we have seen in these markets as they already are the top issuer of new credit cards in both markets. The launch of the deposit-taking products in these markets will likely accelerate growth in customers in the region and I expect this to happen in 2023.

As you can already start to notice, there is a flywheel effect going on as new products will help to drive growth in new markets which will in turn provide more customers for different types of innovative products.

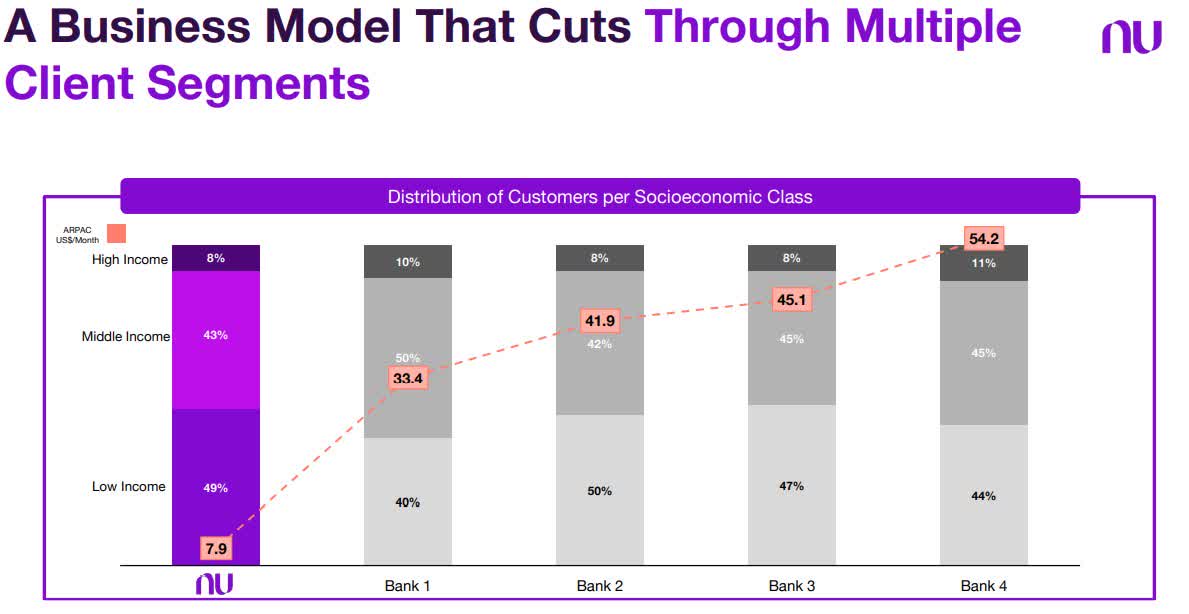

Lastly, Nu seeks to increase its penetration into different client segments in the markets it operates in. The company currently has a similar demographic breakdown to the incumbent banks in Brazil. It has managed to grow its customer base to become fairly similar to the incumbent banks despite the fast growth we have seen in the past years, which continues to show that the company continues to focus on quality growth. This also does illustrate to me that Nu has a strong value proposition and helps with the pain points experienced across client segments.

The next obvious step would be to increase the Average Revenue Per Active Customer (“ARPAC”) to levels closer to the incumbent banks. On average, Nu’s ARPAC was one-fifth that of the Brazilian incumbent banks. This is no doubt a classic upside to value creation through increasing ARPAC to that of the current incumbents through new product launches. Lastly, the high-income group of 8% is in line with the other incumbent banks and will help provide a diversification effect when the macroeconomic environment weakens.

Business model: Client segments (Nu IR)

Best-in-class engagement metrics

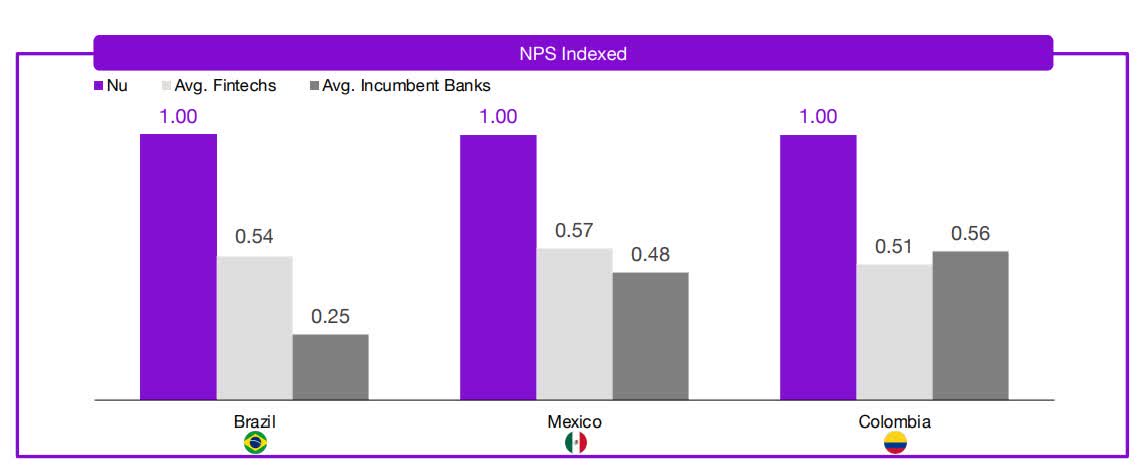

The strong evidence of Nu’s innovative products meeting expectations and removing pain points is through its strong net promoter scores, as can be seen below. When indexed next to Nu’s strong net promoter scores in Brazil, the average fintech had net promoter scores half that of Nu and the average incumbent banks had net promoters scores on average a quarter that of Nu. This illustrates strength of Nu’s innovative products, offerings, and platform over not just incumbent banks but also over fintech companies that are supposed to be bringing new, innovative products to the market. The trend is similar in Mexico and Colombia, where Nu continues to have strong customer satisfaction and best customer experience relative to the average fintech and incumbent banks. This best-in-class net promoter score also brings marketing benefits as almost 70% to 80% of Nu’s 70 million customers were organically acquired through word-of-mouth.

Net Promoter Score of Nu Indexed (Nu IR)

In addition, there is a continued strength and growth in Nu’s DAU/MAU metric as it has reached almost 52% in the third quarter of 2022. This metric is typically a metric used by social media companies and the leading social media companies have on average more than 50% DAU/MAU. While Nu is largely a digital financial services player, the strong engagement on the platform does bring long-term opportunities beyond financial services.

DAU/MAU evolution (Nu IR)

Individual business segments

Nu’s card business continues to grow with the 75% increase in purchase volumes. A large majority of the credit card book comes from existing customers as these older existing customers continue to increase credit card spend on the platform as they spend more time on the platform. For example, Nu states that customers that have been with Nu for 2 years usually triple the credit card spend on the platform on average. As the new cohorts mature, this should also bring new market share gain opportunities for the card business.

The company’s consumer finance portfolio, which includes credit cards and personal loans, grew 83% year on year, accelerating despite 2 headwinds. The first is negative foreign exchange fluctuations, and the second being that originations of personal loans were contained at levels similar to past quarters. I have mentioned in the previous article that Nu looks to increase the resilience of its credit portfolio and as a result, is moderating origination to ensure that originations in the near-term remain stable. The only bottleneck, at least in the near term, for the personal loan business is the company’s own risk appetite. In my opinion, Nu is taking the right step to ensure that it remains prudent during the weak macroeconomic conditions and uncertain times.

Cost advantages

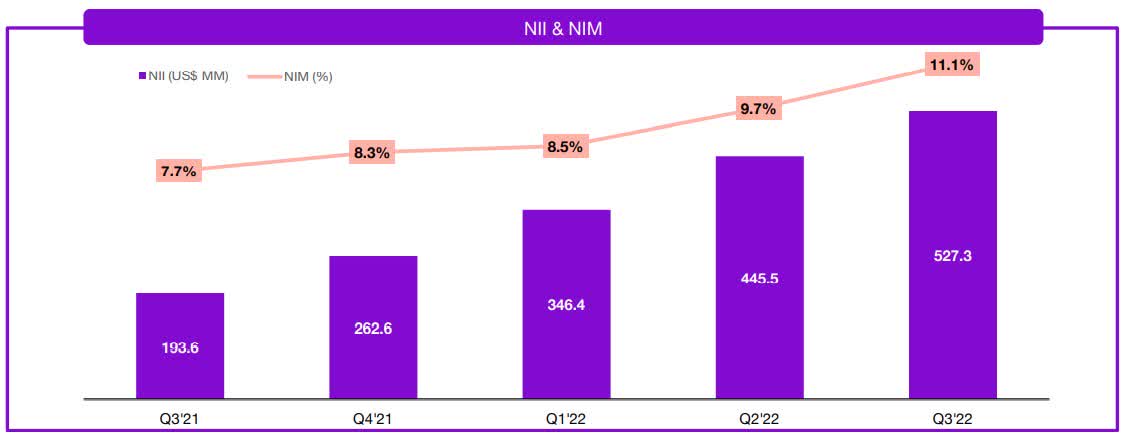

As loans continue to outpace deposits and funding costs are optimized, we continue to see improving net interest income and net interest margins.

Net Interest Margin (Nu IR)

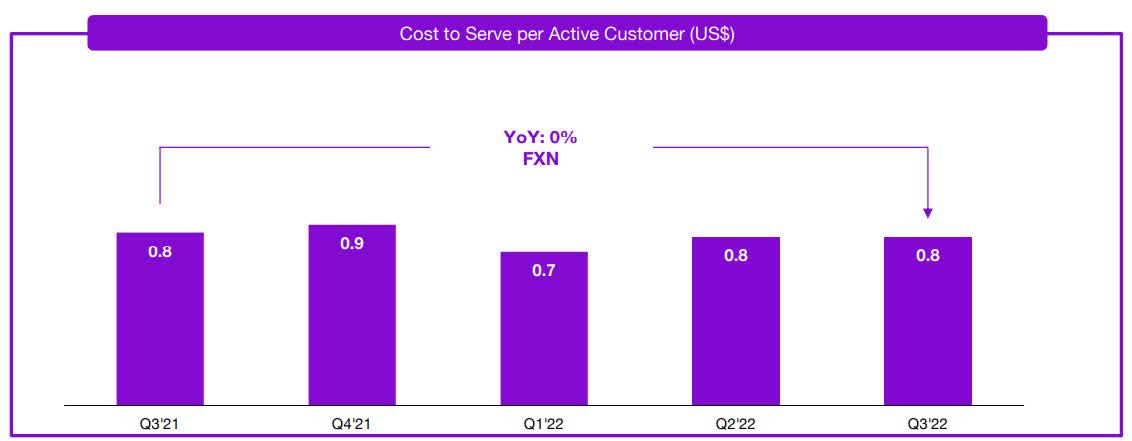

Low cost to serve continues to be one of Nu’s key competitive advantages. As highlighted earlier, the strong net promoter scores as a result of high customer satisfaction remain to be a strong marketing tool for Nu as its customer growth comes from organic sources through word of mouth. While customer and revenue growth continue to be resilient and strong, the cost to serve has essentially been stable from the prior quarter. At $0.80 average monthly cost to serve, this has been maintained since the third quarter of 2021. I expect that Nu will continue to enjoy low cost to serve that will enable significant operating leverage from improving scale.

Nu’s cost to serve per active customer (Nu IR)

The operating leverage of the business model continues to be strong and remains to be a key focus for management. Its efficiency ratio reached 55% in the third quarter of 2022, compared to 92% in the prior year. With slower hiring pace in the coming quarters, I think that this positive downward trend for Nu’s efficiency ratio will continue in the quarters to come.

As highlighted before, profitability is in the minds of Nu’s management team and it generated profits in the third quarter of 2022 as a result of strong customer engagement and the improving operating leverage of its platform.

Valuation

I use both DCF and comparable based methods to derive my target price for Nu. The peer group I used for Nu includes the companies with exposure to digital banks, super apps, or exposure to Latin America. The peer group trades at a multiple range of 5x to 11x 2023 revenues. I think that Nu should have a premium valuation compared to its peer group as a result of a stronger execution, solid management team and continued revenue and profit growth. Nu is currently trading at 2x 2023 revenues, with a 3-year revenue CAGR of almost 40% In addition, my discount rate assumption for Nu is 17%. The higher discount rate used was a result of the rising rate environment. My target price for Nu is $7.80, implying 120% upside from current levels.

Risks

Macroeconomic environment

Nu’s key market in Brazil continues to be a country in which volatility and economic uncertainty is a key risk and headwind. The inflation in Brazil rose to levels not seen in the past 26 years and the economy looks to be vulnerable in this weak global macro backdrop. In addition, volatility in the Brazilian real could also be a near-term headwind if it worsens or goes out of hand.

Competition

The financial sector in which Nu has been operating in continues to be dominated by large incumbent banks while new emerging fintech startups are coming up with new innovation and technology. Nu needs to make sure that its platform remains relevant in a world with strong competition to ensure that it emerges at the top of it.

Conclusion

While the stock price of Nu remains weak, its fundamentals are actually improving. I think that this Buffett-backed fintech player could be the one to watch in 2023 as it continues to execute its business segments well. In my opinion, the company could scale up profitability fairly easily and continue to see revenue growth through multiple sources, as highlighted earlier. The company has low cost to serve and cost advantages that enable it to have a better margin and profitability profile than peers. My target price for Nu is $7.80, implying 120% upside from current levels.

Author’s note: I am starting a marketplace service, Outperforming the Market, which will be launching on 10 Jan 2023. Outperforming the Market aims to help investors identify high conviction growth and value stocks to form a barbell portfolio that outperforms the market.

Mark your calendars, because early subscribers can reserve a spot as a Legacy Discount Member, which gives you generous introductory prices. Thank you for reading and following my work. See you there!

Read More…