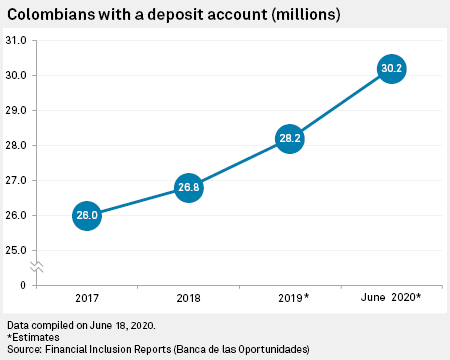

More Colombians have opened their first bank account during the coronavirus pandemic than in all of 2019, with the distribution of emergency welfare driving the country’s latest banking growth spurt.

Collaboration among the public sector, banks and financial technology firms has led approximately two million people to open deposit accounts for the first time between March and the end of this month, according to estimates from Banca de las Oportunidades, a government institution focused on financial inclusion.

This is far above the estimated total of 1.4 million who signed up for their first accounts in all of 2019, Freddy Castro, head of Banca de las Oportunidades, told S&P Global Market Intelligence.

A new requirement for individuals to provide a bank account in which to receive pandemic-related aid from federal, departmental and municipal governments has been the main motive behind the spike in the country’s banked population, according to Andrés Mauricio Ramirez, director of digital transformation and financial inclusion at Colombia’s Asobancaria banking association.

The banking association has been working closely with the National Planning Department and its SISBEN [social assistance targeting tool], which has a database of approximately three million Colombians who receive benefits from the government.

Government officials have proactively notified unbanked sectors that they would now need a bank account or financial application in order to receive support during the crisis, Ramirez said.

Through the national government’s Solidary Income scheme alone, 950,000 people have opened their first accounts to receive 160,000 pesos per month as of June 12. Ramirez highlighted that 50% of these newcomers kept their funds in their digital accounts, either to spend electronically or for saving purposes.

The welfare scheme has benefited a total of 2.4 million families up to June 16, according to its official website.

In a further bid to contain contagion, pensioners who were previously being paid in cash have also been required to open accounts to collect during the pandemic.

“If you add up those who have banked themselves due to Solidary Income, municipal and department level benefits, pensions, and those entering the financial system out of their own initiative, you get two million newly banked Colombians,” Banca de las Oportunidades’ Castro explained.

Most newcomers have signed up for digital solutions provided by Bancolombia SA, Banco Davivienda SA and Grupo Aval Acciones y Valores SA, the country’s largest banks, although financial technology companies such as Movii have also been instrumental in this process, Asobancaria’s Ramirez noted.

A database for the future

Davivienda Vice-President of Personal Banking Products Margarita María Henao Cabrera told S&P Global Market Intelligence that Daviplata, the bank’s e-wallet platform, has seen its client base expand by 3.4 million clients in 2020 to 9.5 million, more than three times the total growth it saw in 2019.

In April alone, one million clients downloaded the app — including more than 100,000 previously unbanked recipients of Solidary Income — as social benefits became a significant driving force behind account growth.

Previously unbanked clients have been digitally paying for utilities and topping up their cell phones, Henao Cabrera said, adding that Davivienda is gradually starting to offer them micro-insurance and micro-credit products. Overall, transactions within the app have soared by 600% since the start of the pandemic, she noted.

“We’re doing everything we can for them to stay on once this [pandemic] blows over,” she said.

For Andrés Márquez, senior director for Latin America financial institutions at Fitch, although most Colombian banks are currently primarily focusing on refinancing their existing portfolios, they are looking for ways to offer more products to newly banked clients further down the line.

“This is how credit histories are started,” Márquez said, adding that “larger banks have prepared their digital channels very well” and have expanded their databases.

Once the pandemic ends, “we’ll see what strategy banks have,” he added, also noting he sees “an opportunity for fintechs to start offering credit to these segments of the population.”

Enter the fintechs

Fintechs have played a complementary role in the expansion of financial services and are now trying to capitalize on new opportunities, according to Edwin Zácipa, co-founder of Colombia Fintech.

As an example, fintechs provided the infrastructure for Venezuelan migrants with temporary residency permits to open accounts and receive benefits from the Colombian government, while traditional banks did not.

While banks have been growing increasingly cautious in the disbursement of new credit lines, many fintechs were quick to raise capital and start lending more, he added.

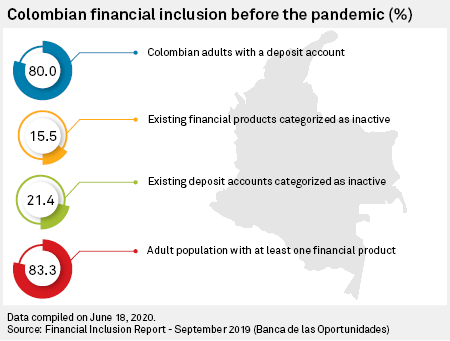

“We’re close to a financial inclusion rate of 85% of the population, which shows that the problem in Colombia today isn’t really one of access, but rather of usage of financial services,” Zácipa said.

But the sustainability of people’s increased use of financial products after the pandemic remains uncertain. “In Colombia we have a huge cash overuse problem, along with a massive informal sector and abundance of loan sharks, and fighting against that is very difficult,” he said.

A more efficient integration of financial services with lower fees and fewer taxes could be an incentive for people to stay within the system, as opposed to opting for an informal cash economy, Zácipa noted.

The relative success of Colombia’s recent approach to financial inclusion during the pandemic could be a model for other countries in the region. Argentina’s government has taken similar measures to do away with cash subsidies, while Mexico has also seen an uptick in digital payments.

READ MORE: Sign up for our weekly coronavirus newsletter here, and read our latest coverage on the crisis here.

As of June 22, US$1 was equivalent to 3,730.50 Colombian pesos.

Source : From the Web